Downtown Apartment Boom Rolls on, but Developers Pull Back

- Posted: August 21, 2019

- better construction, Chicago Construction Market

For a while, it looked as though apartment developers in downtown Chicago would play their predictable role, letting their exuberance get the best of them by overbuilding. But the downtown construction boom is slowing down, according to a new forecast from Integra Realty Resources, a consulting firm.

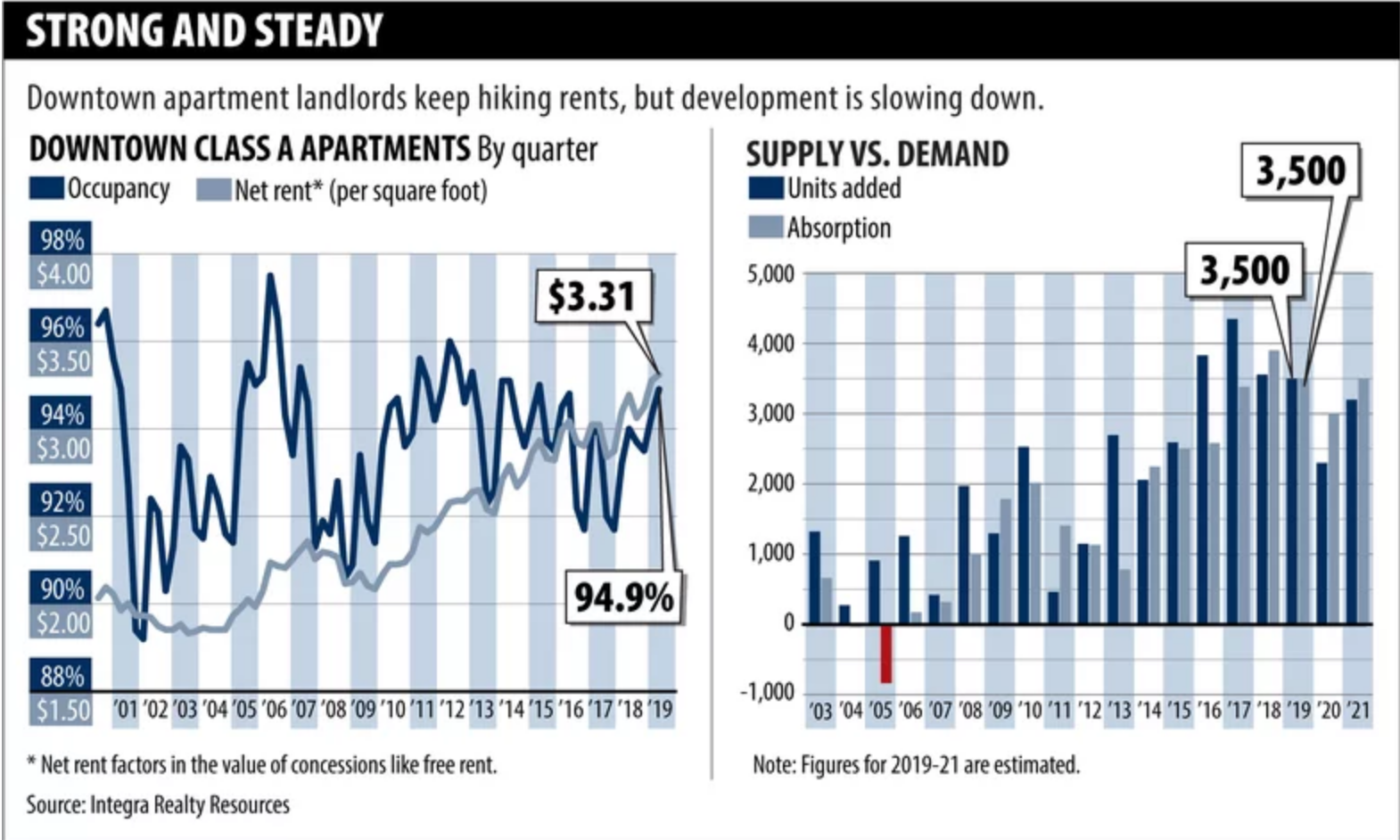

Developers will complete 9,000 downtown apartments in 2019, 2020 and 2021, down from a projection of 10,700 earlier this year, according to Integra. Development is slowing due to rising construction costs, tougher affordable housing regulations and worries about rising property taxes, said Ron DeVries, senior managing director in Integra’s Chicago office.

But one key measure of demand, absorption—or the change in the number of occupied apartments—isn’t quite as strong as it was last year, when it hit a peak of 3,902 units. Downtown absorption totaled 1,351 units in the second quarter, well below Integra’s projection of 1,700, leading the firm to reduce its forecast for the year to 3,500 this year and 3,000 in 2020.

That’s typically a sign of falling demand, but DeVries attributes the recent decline to falling supply: Fewer new apartments result in fewer new leases. Future demand will also depend heavily on the direction of the economy, which is slowing after a prolonged expansion. Rents and occupancies would likely decline should the economy dip into a recession.

For now, however, new buildings are filling up quickly. The Paragon, a 500-unit high-rise at 1326 S. Michigan Ave. in the South Loop that opened in May, is 33 percent leased, according to Integra. The Mason, a 263-unit project at 180 N. Ada St. in the Fulton Market neighborhood that also opened in May, is 70 percent leased.

Downtown development peaked at 4,348 apartments in 2017, dropping to 3,556 last year. Earlier this year, Integra forecast that supply would rise again by 4,100 units.

But developers are dialing it back, and DeVries has revised his supply forecast down to 3,500 units and 2,300 next year. They’re having a harder time securing financing, mostly from equity investors, according to Integra. Rising construction costs have depressed investment returns, as have stricter regulations in some areas that require developers to include affordable housing requirements in their projects.

Some investors also are steering clear of new Chicago apartment projects amid concerns about the city and state’s fiscal troubles. They are certain that property taxes, a key expense for landlords, will rise as a result, but they are uncertain by how much. Adding to the uneasiness about Chicago, new Cook County Assessor Fritz Kaegi has been reassessing commercial properties at much higher values.

“There’s a lot more risk in the market,” DeVries said.

But landlords still have pricing power. Rents at Class A downtown buildings that have been open for a year or more rose 3.6 percent in the second quarter from the year-ago period.