Could Chicago’s Construction Slow?

- Posted: January 15, 2020

- Chicago Construction Market

Chicago’s development party started to wind down at the end of the last decade. The new one may bring the hangover.

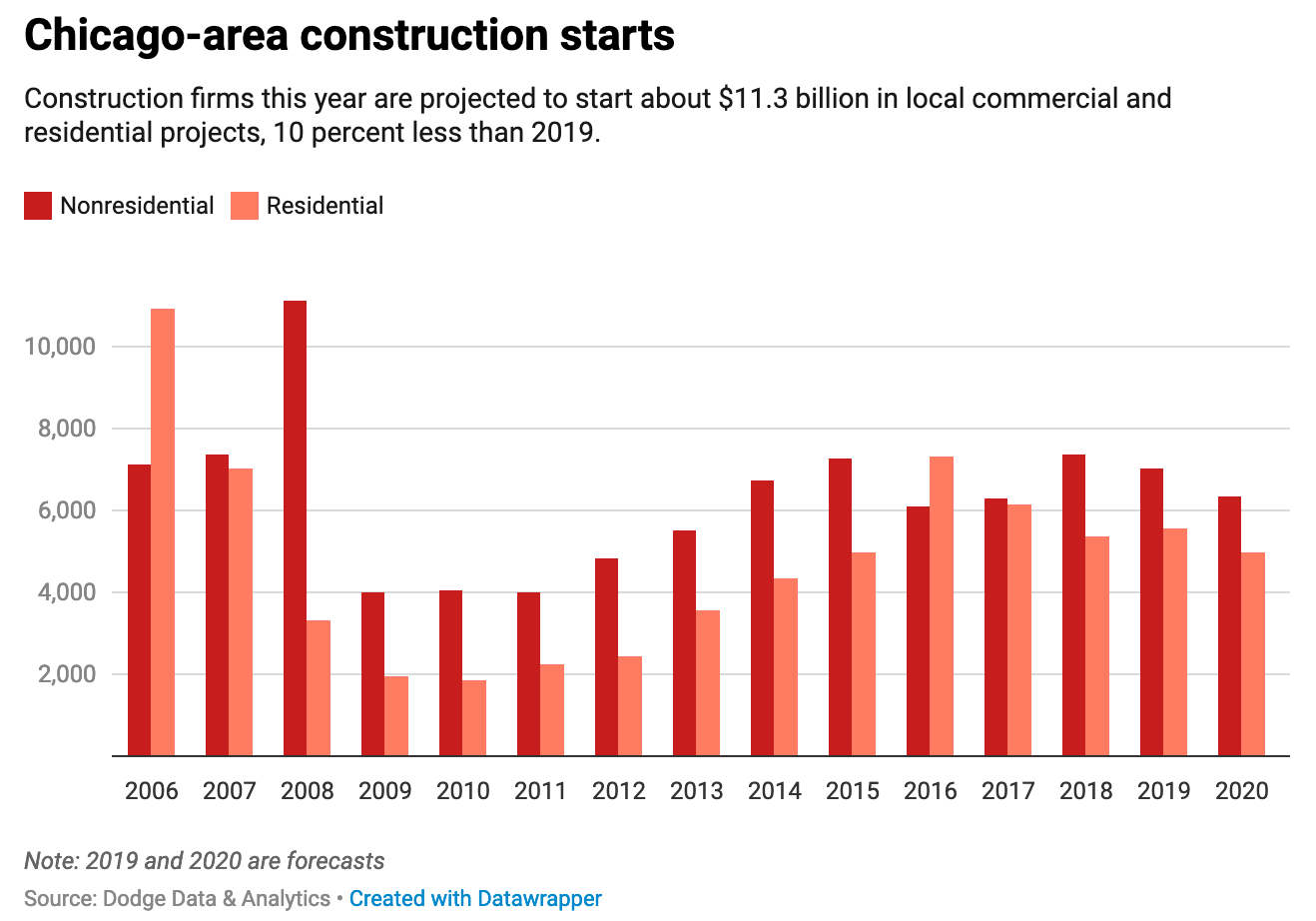

After a building boom that has stretched the boundaries of downtown and put a record number of cranes in the air, new construction projects are forecast to fall 10 percent this year, according to New York-based research firm Dodge Data & Analytics. If that prediction is right, it would mark the third annual decrease in four years and the biggest single-year drop in construction starts since the Great Recession.

It’s hard to see such a slowdown coming when looking around the city today: Demand for office space just capped off its best year since 2007, apartment rents are pushing record highs and developers can’t seem to build enough industrial space to satisfy retailers’ voracious storage space appetite as more people shop online.

But deep into the nation’s longest period of economic expansion—and with lessons of the last market crash still top of mind—developers and real estate investors are signaling they’re not sure how much more room there is to grow.

“I spend every day talking with capital partners and trying to sell them on (new projects in) Chicago, and this has been the most challenging time that I can remember,” says Michael Newman, president of Chicago developer Golub, whose firm is redeveloping Tribune Tower and has been among the most active in Chicago real estate over the past decade.

Golub is stepping up its work in other markets, including Denver and around the Southeastern United States, but has no new Chicago projects slated to break ground this year or the first half of next year. It’s not that they’re afraid to, Newman says. Big financial partners are more reticent to back projects as headwinds pick up for landlords.

“The markets aren’t shut off fully, but there are many investors we work with saying, ‘Let’s wait a little bit to see how some of this shakes out,’ ” he says.

There are macroeconomic challenges holding up new projects—a presidential election year, global economic unease and the threat of new tariffs and trade wars, to name a few. Then there are the even tougher local obstacles: Real estate investors are flummoxed by an overhaul of how Cook County values properties and what that means for property taxes, and tighter affordable housing policies stand to hamper the boom in new apartment developments. Dodge predicts a 24 percent reduction in starts of new multifamily buildings, which drag down the forecast along with a projected 39 percent decrease in new health care construction and a 14 percent drop in new warehouse development.

A substantial slowdown in new projects on top of plummeting commercial property sales last year would indicate that real estate investors think the best days of the current economic cycle in Chicago have passed.

“I think developers and investors have developed a very dim view on Chicago and will maintain that perspective for the foreseeable future,” says John Murphy, whose firm is transforming the former Cook County Hospital into a dual-brand Hyatt hotel and medical offices. “It’s really unfortunate, because the fundamentals for growth are there.”

Dodge forecasts that new construction will still be relatively strong in Chicago, despite the expected decline outpacing the projected national 4 percent drop-off.

Falling to $11.3 billion in new Chicago-area projects would still put the city a little ahead of where it was in 2014. And tower cranes will still dot the skyline for the foreseeable future as new skyscrapers recently got underway along Lake Shore Drive, next to Union Station and across the street from Holy Name Cathedral in River North.

“Chicago is still a relatively healthy market,” Dodge Chief Economist Richard Branch says. “It just really boils down to that uncertainty causing a bit of a pullback over the levels we’ve seen over the past couple years.”

LOADS OF WORK

Construction workers are as busy as ever today, and contractors can’t bring in enough apprentices quickly enough to meet the workload in northern Illinois. More than 200 retirees were tapped last summer for jobs running heavy equipment on construction projects in the area, the most for any year on record, according to International Union of Operating Engineers Local 150.

“The work has been endless,” says Niko Simrayh, an operating engineer at James McHugh Construction who has worked tower cranes for several new West Loop buildings and is now working on the latest additions to the Lakeshore East neighborhood. The 27-year-old estimates he averaged almost 60 hours per week for the past two years and has a handful of new jobs still to come in 2020.

“It’s hard not to assume it’s going to slow down in the next handful of years, but (these days) it’s hard to go more than a month in the West Loop without seeing a new crane go up,” he says.

But the lack of available labor stands to put a clamp on big new projects, as so many skilled workers are already busy. Higher labor and materials costs make it even harder for new developments to pencil out financially.

Chicago had about 130,000 active construction jobs most of last year, up from a low of 104,000 in 2012, according to Moody’s Analytics. The current employment level is still well below the nearly 160,000 jobs just before the Great Recession, but the local capacity shrank after many contractors went out of business after the collapse.

Not all developers have waning confidence about new groundbreaking ceremonies in 2020. Chicago-based North Wells Capital began work in the fall on a 45,000-square-foot expansion of an office building at 306 W. Erie St. in River North and plans to break ground on a 154,000-square-foot office building at 311 W. Huron St. this year, says CEO Jim Fox. Dodge’s forecast backs him up: The firm projects new office construction will actually increase this year by 23 percent.

“We don’t think we’re headed toward being significantly oversupplied” in the office sector, Fox says. He admits property tax uncertainty and city and state budget deficits that could lead to higher taxes are spooking capital partners, but they’re not scaring off new tenants.

“I wouldn’t say things are going to continue unabated” with new office projects, he says, “but Chicago continues to enjoy a lot of strong inbound migration.”